Obtaining a business loan in the United Arab Emirates (UAE), Dubai, Abu Dhabi, Sharjah, or any of the Emirates can prove to be a game-changer in the growth, expansion, or working capital of your company.

However, lenders will insist on a transparent and well-documented set of records that shows that your business is legal, financially sound, and has the ability to repay the loan before they agree to disburse the money.

Incomplete or missing paperwork is one of the leading causes of application delays or outright rejection. This guide explains the documents required for business loan in UAE and what you are expected to present when seeking a business loan in the UAE and the reason why it is a requirement.

1. Legal & Registration Documents

The first thing you should do is to establish your business as legal and registered in the UAE. Most banks and other financial institutions will require the following:

Trade License

An authentic UAE trade license (mainland or free zone) bearing your business name and approved operations. This is the minimum prerequisite of any business loan.

Articles of Association (AOA) & Memorandum of Association (MOA)

The documents show the ownership structure, shareholders, and internal regulations of your company, vital information that lenders require to know who owns and manages the business.

Board Resolutions and Shareholder Certificates

In case your business has more than one owner or partners, you will require share certificates and any board resolution endorsing the loan. These explain authorized signatories and decision-making power.

Power of Attorney (POA)

In the case where loan documents are being signed by a person other than the owners on behalf of the company, a legal POA needs to be provided.

2. Personal Identification Documents

When seeking a business loan, the banks need to have identification documents of all business owners, partners, and directors, as well as the authorized signatories. Generally, you must present copies of authentic passports of all involved people. Emirates IDs and valid residence visas are also required for UAE residents.

These documents aid banks in completing KYC (Know Your Customer) processes and confirming applicant identity, legal ownership, and status. The provision of correct and current IDs will guarantee an easy flow of loan transactions.

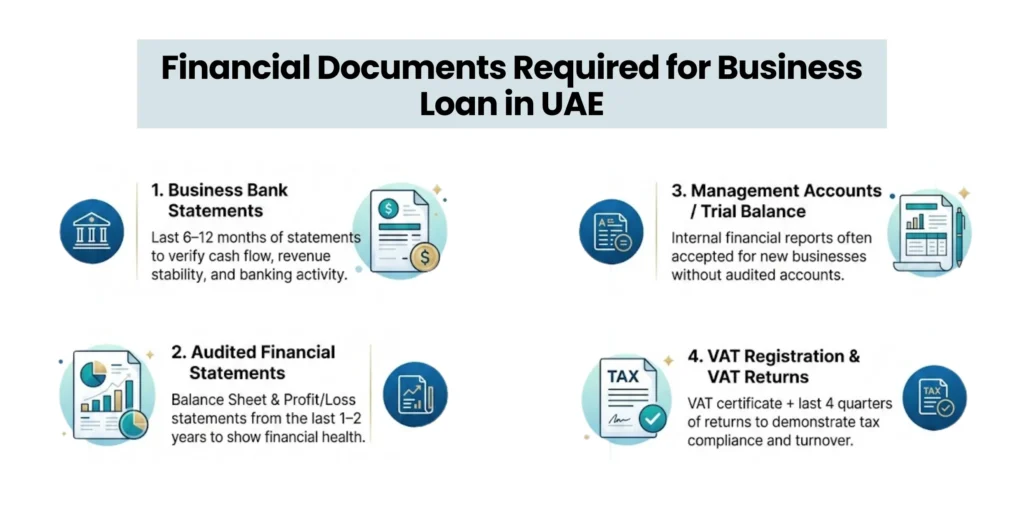

3. Financial Documents Required for Business Loan in UAE

Lenders would want to know that you are sound financially and able to pay the loan. The better your financial documentation, the more a bank will be convinced.

Business Bank Statements

A majority of the lenders will require the past 6-12 business bank statements. These assist in confirming your cash flow, revenue stability, and bank behavior.

Audited Financial Statements

Where possible, audited annual financial statements (balance sheet, profit and loss) of the last 1-2 years are credible and assuring to the lenders.

Management Accounts / Trial Balance

Trial balances or internal management accounts are commonly acceptable in the case of newer companies or those with no audited accounts.

VAT Returns & VAT registration

When your business is registered for VAT, provide the VAT registration certificate and the recent VAT returns (generally the last 4 quarters). These indicate compliance with taxes and turnover.

4. Business View and Operation Evidence

Banks would like to know more about the way your business operates than legal and financial documents. You are expected to give a company profile that describes your business background, business, and core business.

A list of clients and suppliers will display with whom you are involved and your source of revenue. Moreover, major project contracts and invoices reflect the continuity of business and future revenue and aid lenders in evaluating your business strength and repayment ability.

5. Office and Location Documentation

Banks would require evidence of where you can do business. In the case of companies that have physical offices, a legal Ejari or tenancy agreement displays your leased office area. In some cases, you are also asked to provide your recent utility bills that are related to your office address.

These documents ensure that your business has a real, traceable business location. Office documentation of proper and updated records is a way of giving the lenders confidence in your business structure, and the loan is granted easily.

Suggested Read:

- Why UAE Banks Freeze Accounts and How to Avoid It?

- Why Your UAE Business Bank Account Application Got Rejected

6. Current Liabilities and Banking Data

Lenders will verify your financial commitments to determine your capacity to service a loan. You might not be able to submit without having available loan statements or credit facilities.

Other debts are reflected in credit card and liability statements. Banks also tend to look at your business credit history by checking the Al Etihad Credit Bureau (AECB). A good credit score will increase the chances of being approved and even securing better loan terms.

7. Collateral and Security Documents (Where Applicable)

In case your business loan is secured, the banks will require documents that indicate ownership of assets being sold. In the case of real estate, submit the title deeds of the property. In the case of machinery, vehicles, or equipment, provide documents of ownership or invoices.

These assets might also require insurance policies. These papers assist the banks to ensure that there is collateral that can repay the loan to the bank in case of default, and thus your loan application stands better, and the chances of approval are high.

8. Business Plan and Cash Flow Forecast (Recommended)

Most lenders (not all, but most) will request a business plan, particularly in the cases of startups or expansionary businesses. This is a plan on how you will utilize the loan, projected growth, projected revenue, and how you will be repaying the loan.

A cash flow forecast will indicate that you have money coming in and going out, so that the lenders will realize that you can pay off the loan. These reports are more valuable to the new business or the one venturing into a new market.

Why Do Banks Ask for These Documents?

Understanding why each category matters helps you prepare strategically:

- Verification of Legal Existence – Banks must confirm your business is legitimate and authorised to operate in the UAE.

- Identity & KYC Compliance – Helps prevent fraud and verifies who is legally responsible for the loan.

- Financial Health Assessment – Lenders analyse cash flows and financial performance to ensure you can repay.

- Risk & Liability Evaluation – Credit history and existing liabilities influence loan terms, interest rates, and approval decisions.

- Collateral Security – If the loan is secured, lenders need proof of asset ownership.

Conclusion

Applying for a business loan in the UAE involves more than just filling out an application form. It requires a well‑prepared and comprehensive documentation package that lenders can use to assess your business’s legality, financial strength, and repayment ability. Understanding the documents required for Business loan in UAE can help you prepare the right paperwork in advance and avoid delays in the approval process.

Knowing and assembling the necessary papers, trade licenses, and financial reports, personal IDs, tenancy, credit records, etc., will not only make the loan procedure less complex. But you will also be more likely to get the funds that your company requires to develop.

Begin collecting these documents early, maintain them well and professionally, and be prepared to produce more documents in case banks seek clarification.